Hawks finally rule the roost at the Reserve Bank (RBA). The 50-basis point increase in the official cash rate to 0.85% was the minimum one could have expected in the current circumstances. Anything less would have been irresponsibility. The largest increase since February 2000 was well overdue.

May’s 25-basis point increase signalled to financial markets the RBA was getting back to “business as usual”. However, today’s inflation, regardless of its origin, requires more than business as usual. The 50-basis point increase was the correct decision, at least for now. The RBA remains meaningfully behind the yield curve. The new cash rate contrasts with the trimmed mean inflation for the year ended March of 3.7% and the 2-year government bond yield of 2.7%.

Governor Philip Lowe says, “Inflation is expected to increase further, but then decline back towards the 2–3 per cent range next year.” Those hoping to see inflation in that range next year should remember the governor’s comments last month. “The central forecast for 2022 is for headline inflation of around 6 per cent and underlying inflation of around 4¾ per cent; by mid-2024, headline and underlying inflation are forecast to have moderated to around 3 per cent.”

Westpac now believes inflation will worsen further. Recall, the official headline rate for the March quarter year-on-year (y/y) was 5.1% and trimmed mean 3.7%. Westpac lifted its December quarter y/y forecast to 6.6% and the trimmed mean to 4.8% on Tuesday.

There are more hikes in the pipeline. “The Board expects to take further steps in the process of normalising monetary conditions in Australia over the months ahead” and “is committed to doing what is necessary to ensure that inflation in Australia returns to target over time.” While espousing the resilience of the economy, the health of household and business balance sheets and the strength of the labour market, there are uncertainties clouding the economic landscape. “One source of uncertainty about the economic outlook is how household spending evolves, given the increasing pressure on Australian households’ budgets from higher inflation.”

I remain cautious. Household savings are not evenly distributed, so $250bn squirrelled away during the pandemic will not be as supportive of consumption as many expect. While housing prices have started to decline, they “remain more than 25 per cent higher than prior to the pandemic, supporting household wealth and spending.” The RBA has a foot in both camps, “while the central scenario is for strong household consumption growth this year, the Board will be paying close attention to these various influences on consumption as it assesses the appropriate setting of monetary policy.”

Lowe’s laundry list of worries extends overseas: The war in Ukraine and its impact on energy and agricultural commodity prices, China’s COVID slowdown and shrinking consumer spending power worldwide as central banks raise rates and shrink balance sheets.

Perhaps the government should ask Ian Macfarlane, the governor of the RBA between 1996 and 2006 to chair the proposed inquiry into the RBA. He knows how to rein in asset price inflation.

Source: www.cnbc.com

The big four banks continue to offer miserable rates in the one-two year time frame. I suggest looking elsewhere than the big four to park savings up to $250,000.

Numerous authorised deposit-taking (ADI) institutions are covered by the Financial Claims Scheme (FCS) for deposits up to $250,000. The FCS is a federal government guarantee which protects depositors against business failure of the ADI. So, there is no difference in the credit risk between Commonwealth Bank and any smaller ADI for deposits up to $250,000.

At the time of writing, there were several ADIs offering meaningfully more attractive rates than the big four with FCS protection. Macquarie Bank is offering 2.75% for 1-year; AMP Bank 2.90%; Challenger’s bank MyLifeMyFinance 2.75%. There are others much more generous than the big four, who are faster than a cheetah when raising lending rates and slower than a garden snail when raising deposit rates. Have they a social conscience?

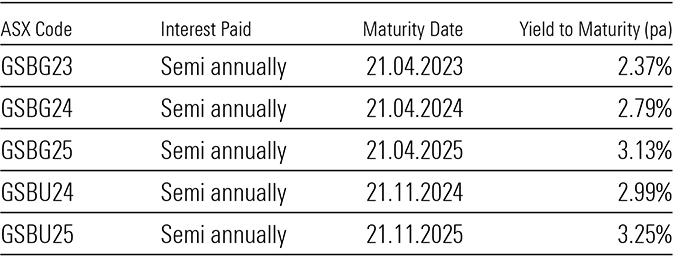

Below is a selection of Australian government bonds that could be considered as an alternative to bank term deposits.

Source: www.cnbc.com

The big four banks continue to offer miserable rates in the one-two year time frame. I suggest looking elsewhere than the big four to park savings up to $250,000.

Numerous authorised deposit-taking (ADI) institutions are covered by the Financial Claims Scheme (FCS) for deposits up to $250,000. The FCS is a federal government guarantee which protects depositors against business failure of the ADI. So, there is no difference in the credit risk between Commonwealth Bank and any smaller ADI for deposits up to $250,000.

At the time of writing, there were several ADIs offering meaningfully more attractive rates than the big four with FCS protection. Macquarie Bank is offering 2.75% for 1-year; AMP Bank 2.90%; Challenger’s bank MyLifeMyFinance 2.75%. There are others much more generous than the big four, who are faster than a cheetah when raising lending rates and slower than a garden snail when raising deposit rates. Have they a social conscience?

Below is a selection of Australian government bonds that could be considered as an alternative to bank term deposits.

Source: Morningstar

Source: Morningstar

1 Detrended using Hodrick-Prescott filter (restriction parameter = 6); adjusted for self-employed income (non-farm business sector, 75% of total economy), from Labor Productivity and Costs database, Bureau of Labor Statistics

Source: BLS (March 2019 release); McKinsey Global Institute analysis

With widespread labour shortages and the number of job vacancies swamping the unemployed, the pendulum is moving in labour’s favour. This is a global phenomenon and one which is likely to persist. In May, US wages increased by 0.31% from April, indicating real wages are flat since pre-pandemic February 2020 and negative since January 2021. Given the elevated global inflation readings, wage demands are unlikely to ease.

Concerted moves to deglobalise and onshore would increase demand for labour in developed economies, keep labour markets tight and light a fire under wages—all likely to be inflationary. As labour demands a greater share of the pie, corporate profits are also being squeezed from other directions.

Tighter conventional and unconventional monetary policy and declining fiscal payments will take the heat out of demand and squeeze operating margins. Higher interest rates and rising business costs will clash with slowing revenue momentum. Pre-pandemic margins were supported by management’s focus on cost cutting, with little juice now left in the lemon.

Companies were lean and mean going into the pandemic and margins have generally improved as monetary and fiscal stimulus pushed demand, with obvious exceptions of hospitality, leisure, and aviation. Now costs are rising rapidly, and demand is destined to lose momentum as tighter monetary policy weaves its spell. This vice-like pincer is likely to subdue earnings growth. Lower economic and corporate earnings growth and higher interest rates are bad news for equity valuations.

1 Detrended using Hodrick-Prescott filter (restriction parameter = 6); adjusted for self-employed income (non-farm business sector, 75% of total economy), from Labor Productivity and Costs database, Bureau of Labor Statistics

Source: BLS (March 2019 release); McKinsey Global Institute analysis

With widespread labour shortages and the number of job vacancies swamping the unemployed, the pendulum is moving in labour’s favour. This is a global phenomenon and one which is likely to persist. In May, US wages increased by 0.31% from April, indicating real wages are flat since pre-pandemic February 2020 and negative since January 2021. Given the elevated global inflation readings, wage demands are unlikely to ease.

Concerted moves to deglobalise and onshore would increase demand for labour in developed economies, keep labour markets tight and light a fire under wages—all likely to be inflationary. As labour demands a greater share of the pie, corporate profits are also being squeezed from other directions.

Tighter conventional and unconventional monetary policy and declining fiscal payments will take the heat out of demand and squeeze operating margins. Higher interest rates and rising business costs will clash with slowing revenue momentum. Pre-pandemic margins were supported by management’s focus on cost cutting, with little juice now left in the lemon.

Companies were lean and mean going into the pandemic and margins have generally improved as monetary and fiscal stimulus pushed demand, with obvious exceptions of hospitality, leisure, and aviation. Now costs are rising rapidly, and demand is destined to lose momentum as tighter monetary policy weaves its spell. This vice-like pincer is likely to subdue earnings growth. Lower economic and corporate earnings growth and higher interest rates are bad news for equity valuations.

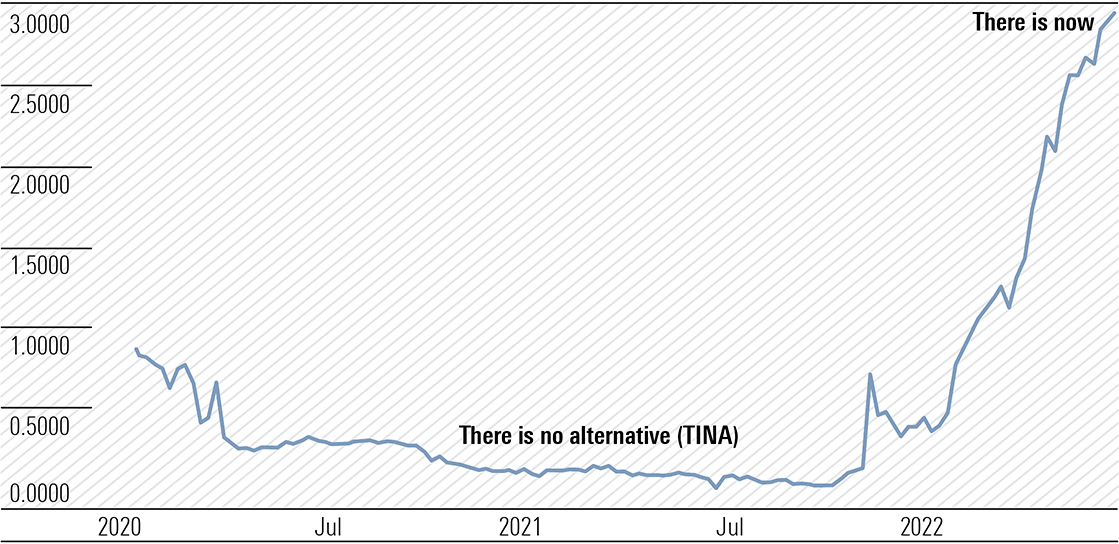

TINA is silent; now There are Alternatives (remember TAA the friendly way)

For years central banks have pushed investors out the risk curve in search of higher returns. There Is No Alternative (TINA) was the rallying cry as investors embraced riskier and riskier assets and altered long-term strategies. But as the winds of change reach gale force, alternatives are presenting. It is time to seek shelter, rein in risk profiles, and widen the margin of safety. Let’s explore what is on offer.Exhibit 1: Australia 2-year bond

Source: www.cnbc.com

The big four banks continue to offer miserable rates in the one-two year time frame. I suggest looking elsewhere than the big four to park savings up to $250,000.

Numerous authorised deposit-taking (ADI) institutions are covered by the Financial Claims Scheme (FCS) for deposits up to $250,000. The FCS is a federal government guarantee which protects depositors against business failure of the ADI. So, there is no difference in the credit risk between Commonwealth Bank and any smaller ADI for deposits up to $250,000.

At the time of writing, there were several ADIs offering meaningfully more attractive rates than the big four with FCS protection. Macquarie Bank is offering 2.75% for 1-year; AMP Bank 2.90%; Challenger’s bank MyLifeMyFinance 2.75%. There are others much more generous than the big four, who are faster than a cheetah when raising lending rates and slower than a garden snail when raising deposit rates. Have they a social conscience?

Below is a selection of Australian government bonds that could be considered as an alternative to bank term deposits.

Exhibit 2: Australian Government Bonds

Source: Morningstar

Bank bulls should take a second look

Conventional thought is bank margins widen as interest rates rise, with lending rates increasing faster than those offered for deposits. There is also the impact of the repricing of fixed and variable loans, with the new rate much greater than any increase in deposit rates offered. However, in the current environment all bets are off. Frustrated depositors could easily become more mobile as more attractive alternatives present. Margins are also likely to take a hit next year when banks need to repay emergency loans from the RBA. At the height of the pandemic, the RBA introduced two major policy responses, the Yield Curve Control (YCC) asset purchases and the Term Funding Facility (TFF). The latter was established to offer low-cost three-year funding to ADIs and had two objectives:- to reinforce the benefits to the economy of a lower cash rate, by reducing the funding costs of ADIs and in turn helping to reduce interest rates for borrowers.

- to encourage ADIs to support businesses during a difficult period, ADIs could access additional low-cost funding if they expanded their lending to businesses. The scheme encouraged lending to all businesses, although the incentives were stronger for small and medium-sized enterprises (SMEs).

The hawks are also flying high in the US

The US Federal Reserve vice-chair Lael Brainard was a confirmed dove. However, her latest comments are hawkish saying, “right now, it’s very hard to see the case for a pause” after the presumed 50-basis point increases in June and July. “We still have a lot of work to do to get inflation down to our 2% target.” Refreshingly, she is a realist and not afraid to move to the more aggressive side of the ornithological see-saw. In last week’s Overview I said, “Bruised investors saw a tentative olive branch in the May minutes of the Federal Open Market Committee (FOMC).” In looking for some respite from a record-breaking run of weekly falls in major US indices, investors bet the FOMC could adopt a wait-and-see approach after two more 50-basis point hikes in June and July, when the federal funds range would sit at 1.75%-2.00%. Some FOMC members, most noticeably Atlanta Fed president Raphael Bostic, have floated the idea of taking a step back in September (there is no FOMC meeting in August) and the May FOMC minutes confirmed such a leaning. Voting hawks now include governors and permanent voting members Michelle Bowman and Christopher Waller, vice-chair of the Fed Lael Brainard and James Bullard (St Louis), Ester George (Kansas City) and Loretta Mester (Cleveland). Chairman Jerome Powell and vice-chair of the FOMC John Williams, President and CEO of the Federal Reserve Bank of New York and a permanent voting member are deemed impartial, but the latter is likely to coo. There are currently two vacant positions on the Board of Governors. It looks like the federal funds rate will settle closer to 3.00% before the current tightening cycle is done with. It will be interesting to monitor the impact when quantitative tightening ramps up from September to US$95bn per month.Decades of margin expansion could be coming to an end as labour demands its fair share

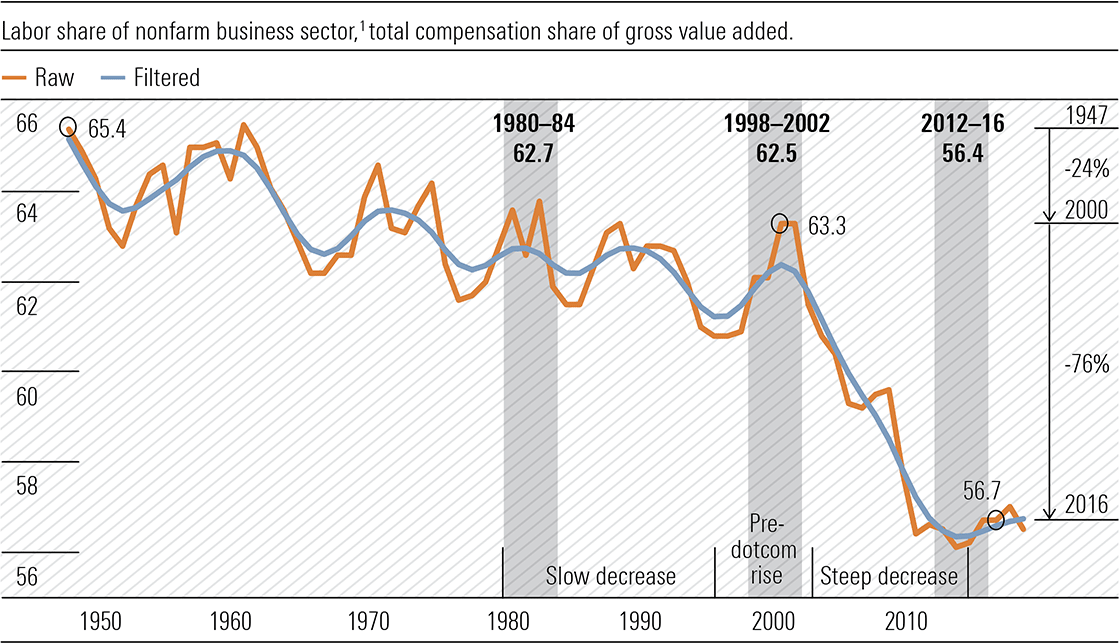

There is a paradigm shift underway and investors should be ready for the consequences. Over the past 20 years capital has been in the box seat and has garnered a disproportionate share of national income on the back of a technological boom, globalisation and monetary policy settings never thought entertainable. But now the worm is turning, and it is labor’s turn to regain some of the lost ground.Exhibit 3: Three-fourths of the decrease in labor share in the United States since 1947 has come since 2000 (%)

1 Detrended using Hodrick-Prescott filter (restriction parameter = 6); adjusted for self-employed income (non-farm business sector, 75% of total economy), from Labor Productivity and Costs database, Bureau of Labor Statistics

Source: BLS (March 2019 release); McKinsey Global Institute analysis

With widespread labour shortages and the number of job vacancies swamping the unemployed, the pendulum is moving in labour’s favour. This is a global phenomenon and one which is likely to persist. In May, US wages increased by 0.31% from April, indicating real wages are flat since pre-pandemic February 2020 and negative since January 2021. Given the elevated global inflation readings, wage demands are unlikely to ease.

Concerted moves to deglobalise and onshore would increase demand for labour in developed economies, keep labour markets tight and light a fire under wages—all likely to be inflationary. As labour demands a greater share of the pie, corporate profits are also being squeezed from other directions.

Tighter conventional and unconventional monetary policy and declining fiscal payments will take the heat out of demand and squeeze operating margins. Higher interest rates and rising business costs will clash with slowing revenue momentum. Pre-pandemic margins were supported by management’s focus on cost cutting, with little juice now left in the lemon.

Companies were lean and mean going into the pandemic and margins have generally improved as monetary and fiscal stimulus pushed demand, with obvious exceptions of hospitality, leisure, and aviation. Now costs are rising rapidly, and demand is destined to lose momentum as tighter monetary policy weaves its spell. This vice-like pincer is likely to subdue earnings growth. Lower economic and corporate earnings growth and higher interest rates are bad news for equity valuations.

Observations

- With headlines screaming ‘gas apocalypse’ the Greens have a solution. The government should subsidise households to ditch gas for electrical appliances, with grants of up to $25,000 and loans of up to $100,000. “Opening up new gas projects is a climate crime.” Switching to electric appliances and electric vehicles increases demand for coal-fired baseload power. Former Energy Security Board chair Kerry Schott fired a warning shot across the Greens bows saying, gas is the crucial link between coal and renewables on the path to zero emissions. “People who want to phase gas out next week are in cloud-cuckoo-land.”

- Australia’s current energy crisis is a wake-up call for those thinking the road to zero emissions is without obstacles. La Nina conditions down the east coast meaningfully disrupted solar generation. Strong to gale force winds sweeping across southeast states are having a similar impact on wind generation. Most turbines are currently tethered. Wind generation requires ‘Goldilocks’-like wind strength—not too strong, not too weak, just right. Both are rightly classified as renewables. They are neither reliable or sustainable and therefore do not qualify as baseload power sources. Time to have the uranium debate and get on with it, just 50 years behind some other countries. It is a dangerous policy to rely on weather-dependent energy sources alone to reach climate goals. Diversity is the key. Germany is now rushing back to the Ruhr after ‘climate’ Chancellor Angela Merkel accelerated the phasing out of nuclear generation.

- Magellan Financial Group has been removed from the S&P/ASX 100 effective prior to the market open on 20 June. A real sign of the times. How the mighty have fallen! The continued decline in funds under management in May has compounded the removal and the share price has tanked a further 14%. When will the Board trigger the 10 million share buyback? The impact is likely to be minimal with turnover of 5 million on 6 June.