The Reserve Bank (RBA) blinked, and markets immediately responded to a less aggressive stance. That does not mean the inflation battle has been won. Far from it, and the RBA’s central forecast for inflation to be “around 3% over 2024” may prove optimistic.

The 25-basis point increase lifts the cash rate to 2.60% and as the board still “expects to increase rates further over the period ahead”, the tightening cycle has been extended into 2023, probably March, with a terminal rate around 3.6%. It is a pity Tuesday’s softer stance was not embraced during the macho Yield Curve Control buying in 2021.

The board would have digested last week’s first monthly indicator inflation data, which revealed the headline rate rose at an annualised 7.0% in July and 6.8% in August, up from the June quarter’s 6.1% year-on-year (y/y) rate. These showed some easing from May and June mostly attributed to a decline in transport fuels. This will reverse sharply in October as the temporary six month 22.1 cents per litre holiday came to an end on 29 September. In addition, a kick up in the oil price, with OPEC+ cutting production from November, will add to underlying pressures.

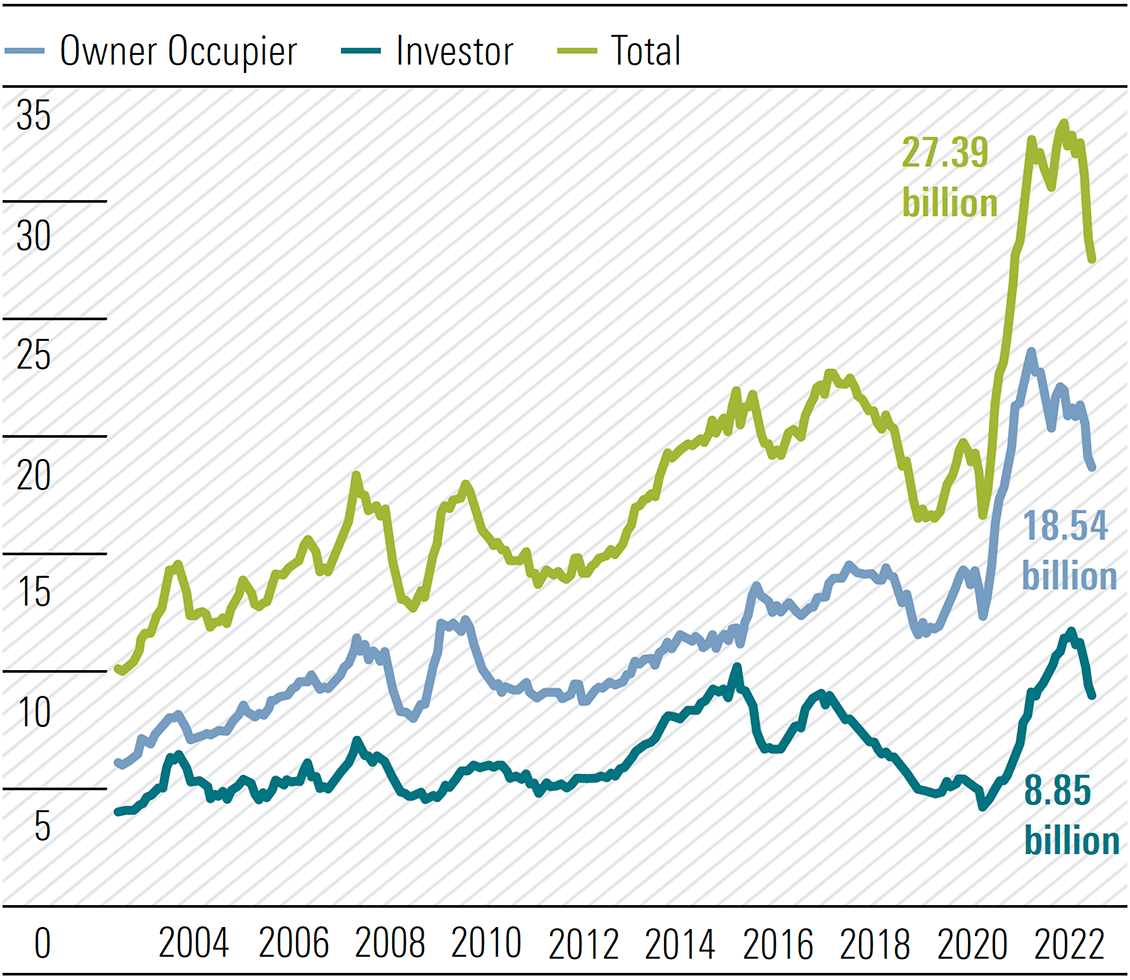

Conditions in the economically sensitive housing sector will also have attracted the board’s attention. Housing loan approvals, excluding refinancing, fell 3.4% in August, slightly worse than expected and on the heels of a sharp 8.5% fall in July. The year-on-year rate is down 12.5% as rate rises impact borrowing capacity and therefore demand. Owner-occupier approvals are down 15.1% y/y, while investor approvals are just 6.4% lower y/y.

Source: National Australia Bank, Macrobond, ABS

Rates have risen a further 75-basis points since end August and housing loan approvals are likely to continue to decline. The environment has seen borrowers abandon expensive fixed rate options, with just 4.4% of approvals fixed, including refinancing, from a peak of 46% in July 2021.

The “data dependent” board will be reading the tea leaves swirling in the housing teacup and the deteriorating market environment will have influenced its moderating decision. Further rate increases will occur, with more legs yet in the tightening cycle. The flip side of reduced borrowing capacity is falling house prices and the associated negative wealth effect.

An unpleasant cocktail of slowing growth in the money supply, monetary policy tightening, and a negative wealth effect is one the RBA board is finding difficult to swallow. Should cracks develop in the labour market the digestion could be even more challenging.

RBA governor Philip Lowe is aware of the uncertainties facing the economy. “One source of uncertainty is the outlook for the global economy, which has deteriorated recently. Another is how household spending in Australia responds to the tighter financial conditions. Higher inflation and higher interest rates are putting pressure on household budgets, with the full effects of higher interest rates yet to be felt in mortgage payments. Consumer confidence has also fallen, and housing prices are declining after the earlier large increases. Working in the other direction, people are finding jobs, gaining more hours of work, and receiving higher wages. Many households have also built up large financial buffers and the savings rate still remains higher than it was before the pandemic.”

In the June quarter, the household savings ratio was 8.7%. However, by September, and almost certainly by year end, the ratio will be below pre-pandemic levels of 7% with household demand finally succumbing to the higher interest rate environment.

September’s Australian Chamber-Westpac Business Survey provided some insight into inflationary pressures yet to be acknowledged in published data.

Source: National Australia Bank, Macrobond, ABS

Rates have risen a further 75-basis points since end August and housing loan approvals are likely to continue to decline. The environment has seen borrowers abandon expensive fixed rate options, with just 4.4% of approvals fixed, including refinancing, from a peak of 46% in July 2021.

The “data dependent” board will be reading the tea leaves swirling in the housing teacup and the deteriorating market environment will have influenced its moderating decision. Further rate increases will occur, with more legs yet in the tightening cycle. The flip side of reduced borrowing capacity is falling house prices and the associated negative wealth effect.

An unpleasant cocktail of slowing growth in the money supply, monetary policy tightening, and a negative wealth effect is one the RBA board is finding difficult to swallow. Should cracks develop in the labour market the digestion could be even more challenging.

RBA governor Philip Lowe is aware of the uncertainties facing the economy. “One source of uncertainty is the outlook for the global economy, which has deteriorated recently. Another is how household spending in Australia responds to the tighter financial conditions. Higher inflation and higher interest rates are putting pressure on household budgets, with the full effects of higher interest rates yet to be felt in mortgage payments. Consumer confidence has also fallen, and housing prices are declining after the earlier large increases. Working in the other direction, people are finding jobs, gaining more hours of work, and receiving higher wages. Many households have also built up large financial buffers and the savings rate still remains higher than it was before the pandemic.”

In the June quarter, the household savings ratio was 8.7%. However, by September, and almost certainly by year end, the ratio will be below pre-pandemic levels of 7% with household demand finally succumbing to the higher interest rate environment.

September’s Australian Chamber-Westpac Business Survey provided some insight into inflationary pressures yet to be acknowledged in published data.

Exhibit 1: Housing finance approvals—excluding refinancing (A$bn)

Source: National Australia Bank, Macrobond, ABS

Rates have risen a further 75-basis points since end August and housing loan approvals are likely to continue to decline. The environment has seen borrowers abandon expensive fixed rate options, with just 4.4% of approvals fixed, including refinancing, from a peak of 46% in July 2021.

The “data dependent” board will be reading the tea leaves swirling in the housing teacup and the deteriorating market environment will have influenced its moderating decision. Further rate increases will occur, with more legs yet in the tightening cycle. The flip side of reduced borrowing capacity is falling house prices and the associated negative wealth effect.

An unpleasant cocktail of slowing growth in the money supply, monetary policy tightening, and a negative wealth effect is one the RBA board is finding difficult to swallow. Should cracks develop in the labour market the digestion could be even more challenging.

RBA governor Philip Lowe is aware of the uncertainties facing the economy. “One source of uncertainty is the outlook for the global economy, which has deteriorated recently. Another is how household spending in Australia responds to the tighter financial conditions. Higher inflation and higher interest rates are putting pressure on household budgets, with the full effects of higher interest rates yet to be felt in mortgage payments. Consumer confidence has also fallen, and housing prices are declining after the earlier large increases. Working in the other direction, people are finding jobs, gaining more hours of work, and receiving higher wages. Many households have also built up large financial buffers and the savings rate still remains higher than it was before the pandemic.”

In the June quarter, the household savings ratio was 8.7%. However, by September, and almost certainly by year end, the ratio will be below pre-pandemic levels of 7% with household demand finally succumbing to the higher interest rate environment.

September’s Australian Chamber-Westpac Business Survey provided some insight into inflationary pressures yet to be acknowledged in published data.

- While manufacturing output rebounded as new orders surged, the survey suggests the reopening effect will fade in the December quarter.

- Costs are still rising sharply driven by labour and material shortages with respondents unable to expand workforces. Conditions in the labour market were the tightest in the history of the series dating back to 1974.

- Input prices continue to increase and combined with shortages, are curtailing the ability of companies to produce at optimum levels.

- The profit outlook deteriorated, impacted by margin squeeze.

- Consumers should brace for further sharp price increases.