Executive Summary

The recent stock market sell-off sees the shares of all of the listed ANZ asset managers we cover trading at substantial discounts. With such fertile hunting ground, we think the market is underestimating the key investment strategies of these asset managers, and their ability to deliver positive alpha and attract money. We think the outlook for asset managers is better than what's currently being priced in. Recent market declines suggest future investment returns will likely improve. Their strong fundamentals, such as having solid operating cash flows and relatively low capital intensity support our conviction.

Key Takeaways

- Magellan is our top pick. We think the market is underestimating Magellan Global's undervaluation and potential to improve its performance. Magellan's efforts to promote its investment team helps assuage key person risks, while selling other better-performing strategies helps mitigate outflows. In CIO Hamish Douglass' absence, Magellan Global remains in the capable hands of co-founder and ex-CIO Chris Mackay, long-time alumni Nikki Thomas, and head of Macro Arvid Streimann. We don’t anticipate material alterations to the Global strategy as all three reaffirmed their commitment to Douglass' investing style (which seeks to invest in companies Magellan thinks have competitive advantages).

- Pinnacle is our second pick. We think the market is overlooking the earnings potential of Hyperion's stocks, performance improvements in boutiques like Antipodes, and its growing asset class diversity. We believe Pinnacle can continue gaining market share from competitors. Pinnacle affiliates are highly competitive, both in performance and fees. It has an expanding product suite that can be tailored to suit varying market conditions. Operating leverage is strengthening as FUM grows.

- Pendal is our third pick. Its recent strong performance supports future flows. Like Pinnacle, its diversified clientele and product breadth expand the channels for new money, and its relatively low fees help it better withstand fee pressure. However, we think Pendal is relatively more vulnerable to outflows from institutional rebalancing and/or platform consolidation activity than Pinnacle.

- Platinum is our last pick. The substantial undervaluation in Platinum’s portfolios supports higher future investment returns. But it is the only no-moat asset manager under our current coverage. Its contrarian investment style suggests future performance can be patchy.

Asset Managers on Sale as Equity Markets Falter

As market-facing investments, shares of asset managers have significantly de-rated as volatility hit equity markets. We believe their prevailing share prices reflect an unduly bearish outlook. Investors appear to be overemphasising short-term downside risks, and underappreciating that capital markets, the performance of many of these strategies, and flows are likely to recover in time.

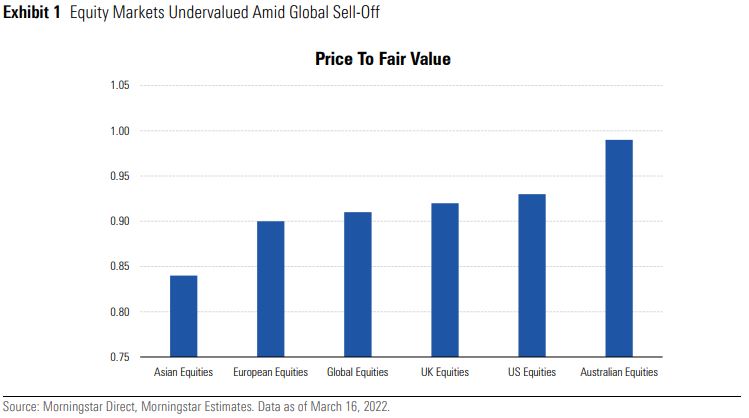

Morningstar analysts collectively expect global equities to grow earnings meaningfully from here. We see lower likelihood of sharp valuation multiple compressions from hereon and this is important to fund returns and manager earnings. Based on Morningstar's assessment, global stocks are already undervalued on aggregate, as seen in Exhibit 1.

This suggests if a constant multiple is applied on higher future earnings, higher share prices (and potentially equity markets) are likely. This bodes well for asset managers who mainly derive revenue by earning a cut of FUM. Recall that global equities fell more than 20% during the pandemic sell-off in February 2020, but the peak to trough decline lasted only two months. Global equities reclaimed their pre-COVID-19 heights in March 2021, around just a year later.

For us to arrive at valuations for Magellan, Pinnacle, Pendal, and Platinum in line with their current prices suggest the market is pricing an average NPAT decline of 6% per year for these firms over the next five years. For this to occur, we estimate they would need to deliver below-index returns, and most continue to bleed outflows. We believe this is unlikely. As we will address below, many key holdings of the biggest strategies of these four asset managers fell materially below Morningstar’s intrinsic assessment. This means there is higher probability for these strategies to deliver abovemarket returns. If this happens as we would expect, it would likely help relative performance and assist with winning new money.

We expect these four fund managers to grow EPS at an average rate of 7% per year through to fiscal 2026, mainly from above-consensus investment returns and leveraging FUM (and revenue) growth over fixed costs. If this plays out as we expect, it would be reasonable to see expansion of the managers' price/earnings multiples to an average of 15 times by fiscal 2026, from an average of 12 times currently, adding to prospective returns for their owners.

We believe the recent asset manager sell-off overlooks some of the attractive traits of these businesses. For example, certain managers like Pendal have delivered extended outperformance, which help support future mandate wins. The compounding potential of fund managers with larger FUM like Magellan, Pinnacle, and Pendal means there is support to earnings from investment returns notwithstanding periodic outflows. Capital management initiatives like share buybacks could also become a feature. Magellan has just announced a share buyback representing up to 5.4% of its shares on issue. Others could follow, like Platinum. We think this reflects the relative cheapness of the shares and a lever for listed managers to boost shareholder returns.

Outlining our earnings forecasts, we expect underlying NPAT for

Magellan to decline at 9% per year over the next three years to AUD 315 million (from AUD 413 million in fiscal 2021), before growing at a 10% CAGR to AUD 382 million over the two years to fiscal 2026. We forecast FUM of AUD 99 billion by fiscal 2026, below AUD 114 billion in fiscal 2021. We expect FUM to be exclusively driven by market returns averaging 15% per year, given the significantly undervalued starting point of the portfolios, and incorporate net outflows totaling AUD 77 billion over the next five years to fiscal 2026. At its current share price, we estimate the market is pricing in ongoing decline in FUM to roughly AUD 53 billion by fiscal 2026, with net outflows totalling close to AUD 90 billion and likely below index returns of 8% per year. We don’t think this is likely as it assumes Magellan will keep underperforming and fail to attract any new money over the next five years.

We forecast underlying NPAT for

Pinnacle to grow at high-teen rates per year to exceed AUD 170 million by fiscal 2026, below the four-year average of 50%. We expect Pinnacle to win inflows at high-single-digit rates (from new clients, product enhancements and boutique additions), and grow affiliate FUM at an 18% CAGR to reach AUD 204 billion by fiscal 2026, from AUD 94 billion at end 2021. At current prices, the market may be pricing in slower FUM growth of 13% to reach AUD 168 billion by fiscal 2026. This assumes much slower growth in market share. We view this as unlikely as Pinnacle is: 1) still expanding the offering and geographic footprint of its affiliates, who are highly competitive in performance and fees; and 2) likely to acquire new boutiques.

We expect

Pendal to grow underlying NPAT at 8% per year to reach AUD 243 million by fiscal 2026, from AUD 165 million currently. We forecast Pendal to grow FUM at a 7% CAGR from fiscal 2021 to reach AUD 196 billion by fiscal 2026, mainly from group returns averaging 10% per year. We forecast net inflows into Pendal’s Wholesale and TSW channels to be offset by outflows from its Institutional and Westpac channels. We deduce Pendal’s share price is pricing in a scenario akin to net outflows across all channels and lower investment returns than historically. This pessimistic assumption negates the fact that Pendal’s near-term performance is supportive of future net inflows, and it now has a greater mix of equities FUM (and lower mix of cash and fixed interest FUM) than historically.

We forecast Platinum's NPAT will stay stagnant at circa AUD 133 million over the next three years, before growing at a two-year CAGR of 9% to AUD 160 million by fiscal 2026. We forecast FUM to grow at a 5% CAGR from fiscal 2021 to reach AUD 30 billion by fiscal 2026. This would mainly be from investment returns averaging 12% per year, above our market assumption given the undervalued starting point for holdings. We expect net inflows to return in fiscal 2025. We estimate that the market is pricing in persistent outflows and below index-investment returns over our forecast period.

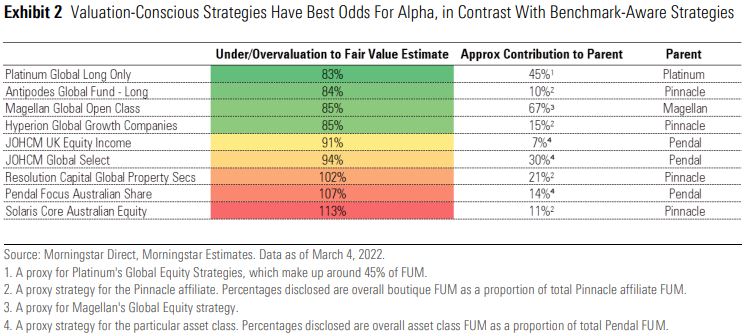

The Greater the Undervaluation, the Greater the Probability to Outperform

Active managers aim to beat the market and protect from downside. To gauge the likelihood of this claim, we think it's useful to assess how under/overvalued a manager's portfolio stock holdings are relative to our assessment of their intrinsic value. In our mind, an asset manager who focuses on filling a portfolio with undervalued stocks shows a value focus, and a discipline to invest in what we think is cheap. If done well, this could support above-benchmark returns.

We assess the relative valuation of the asset managers' key strategies to give an insight into the managers' investment styles. We've taken a close look at the strategies: 1) with higher FUM (and therefore contribute materially to group earnings); or 2) with more concentrated holdings such that the potential for alpha can be assessed.

- Magellan Financial Group: Magellan Global Fund

- Platinum Asset Management: Platinum Global Long Only

- Pendal Group: Pendal Focus Australian Share, JO Hambro (JOHCM) Global Select, JOHCM UK Equity Income

- Pinnacle Investment Management Group: Hyperion Global Growth, Resolution Capital Global Property Securities, Antipodes Global Fund - Long, Solaris Core Australian Equity

As each strategy tends to not disclose its full holdings, we have assessed the top 10 stocks. Excluding JO Hambro (JOHCM), the top 10 stocks make up an average of 48% of FUM across strategies under consideration. For both JO Hambro strategies, we take a weighted average of the

top 20 stocks given their lower concentration in individual holdings.

Intrinsic values of underlying stocks were predominantly drawn from the fair value estimates of Morningstar analysts covering these stocks. For stocks not covered by Morningstar, we have sourced their intrinsic value from Morningstar Quantitative Equity Ratings.

We think it's reasonable to assume over the long run, asset prices converge and those managers with undervalued portfolios are likely to outperform. We also think when the market is relatively cheap, asset managers should expect higher returns in future, and the reverse if the market is expensive.

We think the concentration of undervalued stocks means both Platinum Global Long Only and Antipodes Global Fund - Long could deliver above-benchmark returns over the medium term. We forecast Platinum to deliver returns averaging 12% per year (at the group level) over the next five years to fiscal 2026, unlike consensus which appears to be pricing in index-like returns of about 9% annually. Our base case assumes Platinum's net outflows moderate as its poor relative performance turns around, with net inflows returning from fiscal 2025.

Both firms' investment rationale can take time to unfold, as their somewhat contrarian approach means they need the market to eventually recognise the value in their "out of favour" stocks. Both Platinum and Antipodes are benchmark-agnostic. Both do not shy away from being overweight in pockets that the market perceives to be riskier, such as in emerging markets. The downside risk is if the market does not recognise their contrarian ideas, affecting their chances to outperform and attract fund inflows.

We think Hyperion Global Growth and Magellan Global have strong prospects to deliver abovebenchmark returns over the medium term at current market valuations. We forecast Magellan to deliver returns averaging 15% per year over the five years to fiscal 2026, again defying consensus which appears to price in below-index returns. Both favour companies that can compound earnings growth (and with it intrinsic value), which typically attract higher relative multiples. This investment style paid off well in disinflationary booms, as the expansion in multiples outpaced earnings growth.

However, the rotation into deep value/cyclical stocks starting late 2020 and prospects of rising rates in 2022 sharply de-rated valuation multiples for Hyperion and Magellan's holdings to levels Morningstar considers well below their intrinsic value. We believe both portfolios' above-market earnings growth profile, and the somewhat depressed starting point for the share prices of the holdings, will support re-ratings in time.

We expect Pendal's JO Hambro business to return to net inflows in fiscal 2023 after five straight years of underperformance-led outflows. JO Hambro strategies are value-oriented, and most beat benchmarks in fiscal 2021 as the market favoured deep value and cyclicals. JOHCM UK Equity Income beat its benchmark by more than 30% over the year to September 2021, and we still see some room for alpha. The strategy aims to buy stocks with higher forward yields than the index.

This strategy means the portfolio is generally buying stocks we consider undervalued, as abovemarket dividend yields usually imply "value" stocks trading below market multiples. On the other hand, Solaris Core Australian Equity and Pendal Focus Australian Share consist of

portfolio holdings that are on average most overvalued. Both are more benchmark aware and are style-neutral. Managers are likely mirroring the benchmark in the first instance, and then making tweaks to outpace the index.

Undervaluation Does Not Guarantee Outperformance: Moats and Earnings Power Matter

There is a reason Warren Buffett moved beyond Ben Graham's discipline of strictly buying stocks priced below net current assets. An undervalued company signals the market's concern on the durability of its earnings. Fair value estimates can be wrong if a company does not generate cash flows as estimated, and investors risk buying value traps. We believe underpriced, competitivelyadvantaged companies that can compound earnings consistently are more compelling investments.

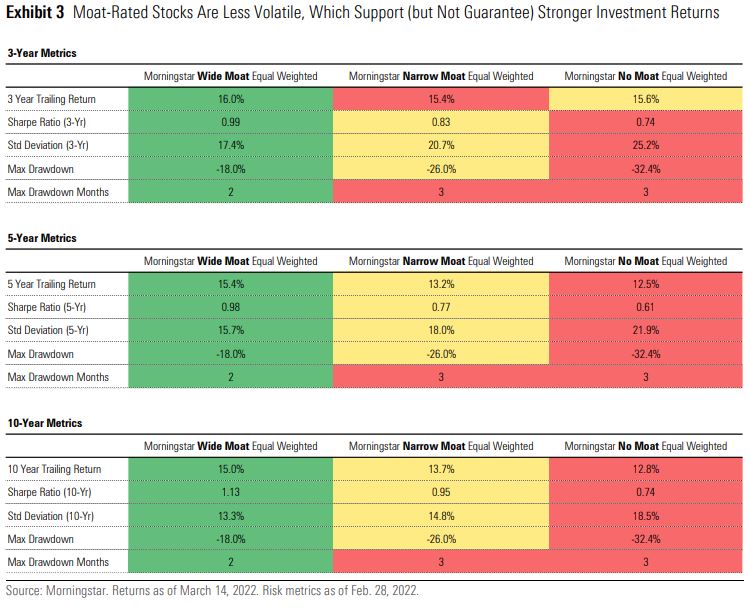

Morningstar’s measure of competitive advantages—the Economic Moat rating—is instructive in this regard. Moaty businesses tend to be better placed to fend off competitive pressures, and generate earnings that are less influenced by market or economic gyrations.

The merits of investing in companies with economic moats go beyond the theory. Per the comparison of performance between the Morningstar Wide Moat, Narrow Moat, and No Moat Equal Weighted indexes below, economic moats were instrumental in helping: 1) companies recoup

earnings faster after a material downside event; and 2) stock prices better withstand market volatility. The ability to compound cash flows should manifest in excess returns on invested capital, generating more shareholder value over time through capital gains and/or dividend returns.

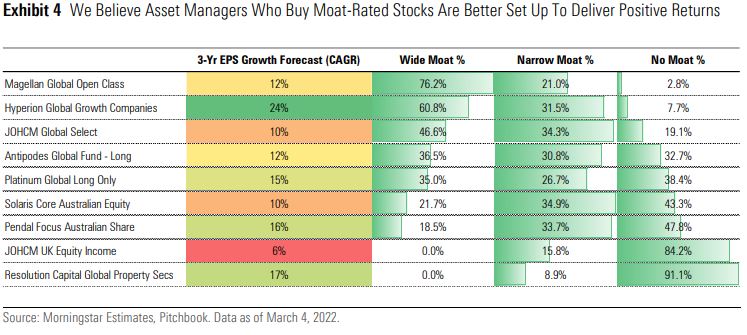

In assessing the asset managers under our ANZ coverage, we first include an economic moat overlay onto their strategies. We then include earnings per share, or EPS, forecasts for the top 10 stocks (20 for JO Hambro strategies) across each strategy, on a weighted average basis. EPS

forecasts are primarily drawn from the projections of individual covering analysts within Morningstar. For stocks not covered by Morningstar, we have sourced consensus data from Pitchbook.

With a portfolio mainly consisting of undervalued, moaty stocks, we believe Magellan Global has the best odds to deliver alpha relative to its benchmark. Morningstar analysts estimate its top 10 holdings to grow EPS at a 12% CAGR (on a weighted-average basis) over the next three to five years, above the expected EPS growth for global equities. The firm looks at competitive advantages, reinvestment potential, and agency risk with the aim to create a portfolio with predictable cash flow and low beta. This approach saw Magellan capture most of the MSCI World’s rise since inception to the end of February 2021. The strategy also appears to offer downside protection, which we attribute to its balance between growth and defensive businesses, holdings in large firms with global operations, and high cash levels. Historically, the portfolios have exhibited lower market drawdowns in times of market sell-offs.

Granted, Magellan Global's weak recent performance has taken some shine off the strategy. Its underperformance over the three months to February 2022, a period of heightened volatility, also meant it failed to protect from the downside here. We acknowledge Magellan made mistakes, but its investing calibre is not broken. We think the underperformance largely reflects Magellan's overweight toward technology stocks, which were sharply de-rated amid the double whammy of rising rate expectations and government crackdowns (as with the case in China). Per Exhibit 2, we think downside risks to its holdings are more than priced in, and don’t anticipate similar sharp detractions to performance over our forecast period. We believe its underlying stocks' earnings power and the durability of their moats will support a steadily compounding earnings stream, supporting a re-rating.

Sitting under the Pinnacle umbrella, Hyperion Global Growth's 47 times price/earnings ratio looks inflated relative to its peer average of 18 times. But this should be viewed in line with the portfolio's expected EPS growth of 24% per year over the next three to five years, outpacing the expected EPS growth for global equities. The fund's research process resembles Magellan, namely, identifying businesses with strong competitive advantages and can achieve high returns on equity.

On the other end of the spectrum lies JOHCM UK Equity Income (under Pendal), with the majority of its funds invested in no-moat businesses. The strategy looks for higher-yielding (relative to the FTSE) companies which, in isolation, might signal potential value traps. We think there is some risk in focusing on yield, as opposed to the moats and durable cash flows. This has been borne out in the historical results. JOHCM UK Equity Income has historically delivered somewhat poor downside protection and drawdown records. The strategy also ranked in top quartile less frequently than most other managers in our sample size (59% of the time over a rolling three-year period, in front of Platinum and Antipodes' long-only strategies but behind everyone else).

Resolution Capital, who invests in REITs, is a unique outlier. Its lack of moatworthy stocks reflects the rarity of moats in the listed property space. Moats are generally hard to come by in REITs as portfolio changes may dilute the overall quality of properties in a portfolio. Alternatively, REITs may acquire properties at a price that makes earning positive economic profits difficult. Excess returns for REITs are typically relatively slim to begin with.

Earnings Growth Helps One Sail With the Wind, Moats Help Minimise Wave Turbulence

Good earnings growth does not guarantee good stock returns as it depends on the price paid and the market expectations at the time. We believe asset managers who seek to own undervalued companies that: 1) have durable competitive advantages; and 2) can generate excess returns on new invested capital have greater odds to achieve outperformance across different market conditions.

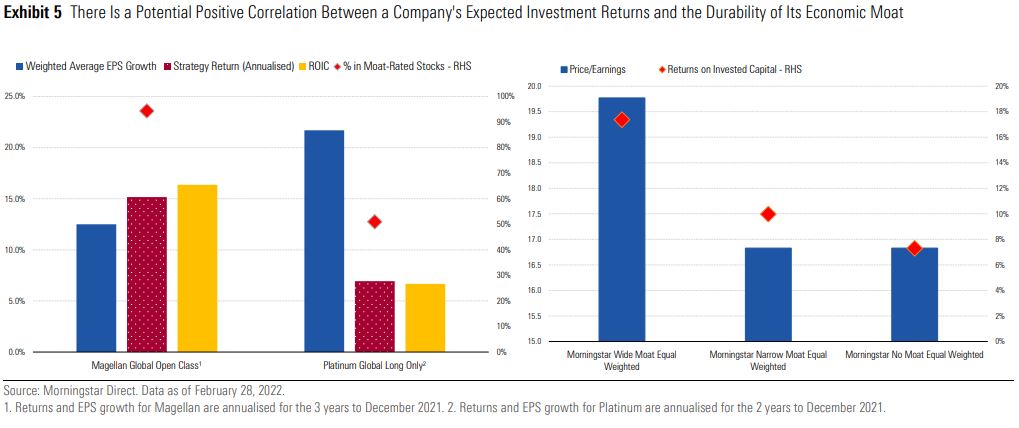

We contend there is a potential positive correlation between a company's expected investment returns from the managed portfolios, and the durability of the firm's economic moat. Illustrating our point, we compare the: 1) actual EPS growth of key holdings in the Magellan Global and Platinum Global Long Only strategies; and 2) their actual investment performance. Using portfolio holdings as of December 2018 (for Magellan) and December 2019 (for Platinum), we have computed their annualised EPS growth (on a weighted average basis) and investment performance over the three and two years to December 2021, respectively.

Note that we use a shorter investment horizon for Platinum given its faster portfolio turnover than Magellan, which would see it realise its investment rationale (and therefore sell/exit positions) sooner.

Despite investing in firms that had higher EPS growth than Magellan Global's picks, Platinum Global Long Only's annualised returns have lagged both its own stocks' EPS growth and Magellan Global's annualised returns. Note that Magellan Global (with twice the amount of FUM invested in moatworthy stocks, relative to Platinum) has eked out annualised returns that exceed its own stocks' EPS growth. This indicates multiple expansion in the case of Magellan, and multiple contraction for Platinum.

Granted, the above comparison is not perfect as it: 1) excludes investment contribution from the rest of the investment portfolio (remember that we only use their top 10 stocks as a proxy); and 2) does not factor in monthly portfolio changes over the investment horizon.

We believe asset managers who look at competitive advantages, and overlay this on top of earnings growth analysis have a greater probability to deliver positive alpha through the cycle relative to their peers.

Past Performance Does Not Indicate Future Returns, but Affects Near-Term Flows and Valuation

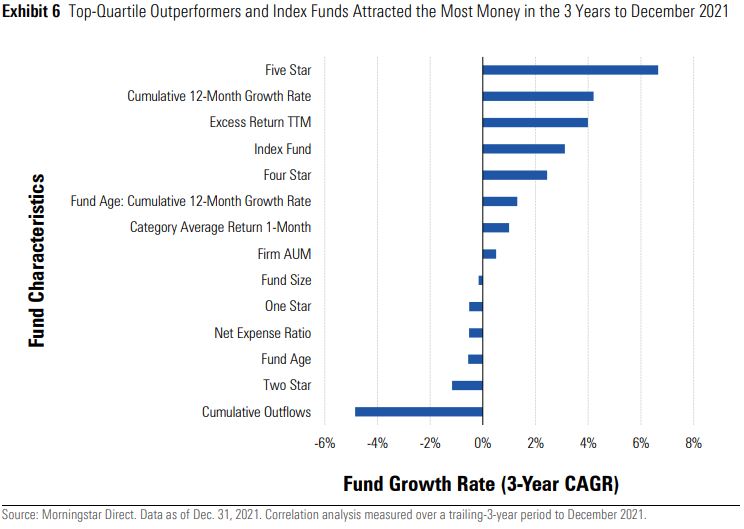

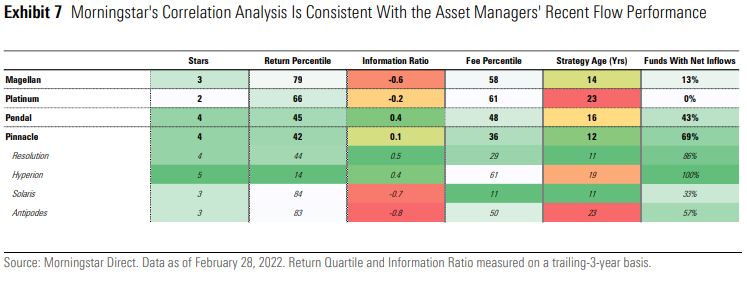

While past performance isn’t a reliable indicator of future performance, investors often consider a manager's historical track record when making allocation decisions. In fact, in the three years ended 2021, a five star backward looking performance rating—which equates to scoring in the top 10% of its category—was the biggest single factor most correlated to fund inflows. The focal points often boil down to simple factors like performance and fees. In general, well-performing fund managers who charge below-average fees have better odds to attract new money, relative to those on the other side of the equation.

Per above, we outline a three-year correlation analysis on global managed fund growth rates and their characteristics, drawn from Morningstar Direct. Our findings suggest strategies with peerbeating performance, index funds—we equate this to low fees, and younger, growing funds—are likely to continue to attract flows at a faster rate than their competitors. On the flipside, older, expensive funds with poor relative performance and presently in net outflows will likely continue to face redemptions.

Both Magellan and Platinum require prolonged improvements in investment performance before net inflows are likely to resume. With their low-quartile ranking and relatively high fees, performance is critical to a turnaround. Positively, we believe both can deliver above-market returns over the medium term. We think the current rotation out of high-growth tech stocks, a headwind on returns for Magellan, will normalise and expect what we now see as undervalued stock picks to converge toward their intrinsic values. For both firms, we forecast elevated net outflows through to fiscal 2024, before moderating. We expect Platinum to enjoy net inflows in fiscal 2025. Our forecast net flows for Magellan and Platinum over the five years to fiscal 2026 amount to negative AUD 77 billion and negative AUD 2.3 billion, respectively. This is about 67% and 10% of their respective FUM as of June 2021.

Magellan Global has beaten its peer average 89% of the time since June 2007 to February 2021. But it has suffered with the market's rotation to deep value/cyclical stocks, which started around early 2021. This coincided with isolated but acute stock mis-steps, notably on Alibaba and Tencent, which fell afoul of a government crackdown on technology firms in China. These events decimated its short and long-term track record by most measures, as seen above. We view this underperformance as a one-off (but damaging) disruption, and do not believe Magellan's investing acumen has diminished. However, we recognise that until Magellan Global outperforms its benchmarks again, ongoing institutional redemptions and CIO Hamish Douglass' leave of absence could see more redemptions. This is undeserved in our view, as we believe there is no fundamental breakdown in Magellan's investment process. Note that interim lead manager Chris Mackay also adopts a parallel investing style to Douglass.

Meanwhile, Platinum's contrarian investment style necessitates the market to also buy into its "outof-favour" ideas to outperform, and for the stock to re-rate. This has often not been the case, per Platinum International's subpar track record since 2014.

Despite Pendal's strong medium-term track record (which should help attract new money), there are some persistent inhibitors to net inflows. For example, outflows from institutional investors inhousing their investment management or diversifying their fund manager exposure, and platform consolidation activity. Pendal is vulnerable to these developments given its maturity relative to newer managers like Pinnacle or Fidante. We forecast Pendal to remain in net outflows at the group level throughout our forecast period. We anticipate net inflows into Australian Wholesale, U.S. Pooled and TSW—its better-performing business channels—to be offset by net outflows from its Westpac, institutional, and U.K. open-ended investment company mandates.

We estimate 43% of Pendal's strategies (by number) are currently experiencing net inflows. This figure could grow so long as Pendal: 1) delivers positive alpha relative to benchmarks; and 2) expands its product range to further extend its relevance to clients. The latter includes Regnan, its suite of ESG products. Pendal's relative performance improved materially after the pandemic sell-off in fiscal 2020, with 83% of FUM in the top quartile over the year to March 2021. This receded to 62% over the year to September 2021 but remains above an average of 44% since fiscal 2016 to first-half fiscal 2020. Its healthy information ratio suggests not only are funds beating benchmarks, but doing so consistently. Fees are trending down as Pendal lowers investment management costs as FUM grow in scale.

We believe Pinnacle, as a holding company of multiple boutiques, has a more resilient business model than standalone boutiques. Notably, its relevance across market cycles is something individual boutiques cannot replicate. We think the firm remains in growth phase, and see it

growing FUM at an 18% CAGR to AUD 204 billion by fiscal 2026, supported by net inflows at highsingle-digit growth rates. The firm's information ratio of 0.1 (at the group level) alludes to Pinnacle's tactic to assemble a list of uncorrelated strategies, so it can adjust the mix of its client offerings based on varying market conditions. We estimate 69% of strategies (by number) are in net inflows.

As a case in point, Hyperion's growth, developed-market-oriented investments stand in contrast to Antipodes' value bias and overweight in emerging markets. This has allowed them both to be packaged and sold by Pinnacle to investors as "equity style hedges."

The strategy works, with around two-thirds of gross sales flow opportunities for Hyperion and Antipodes currently from institutional investors based abroad. Despite being in below-average return quartiles and generating negative information ratios (as seen in Exhibit 7), Antipodes is still receiving inflows into certain strategies.

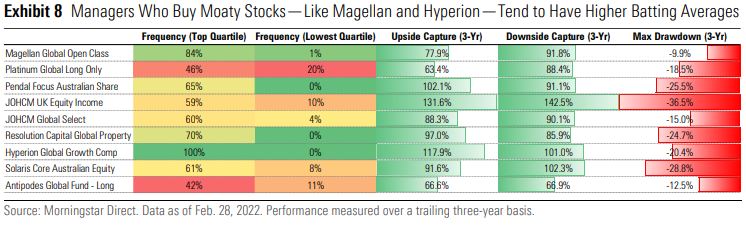

Batting Averages Matter in Measuring Investment Success

The above comparisons are trailing three-year assessments ending as at a point in time and would be skewed by short-term market movements. Investors may need to assess an asset manager's historical performance with more granularity to facilitate a fairer comparison.

We point to two granular performance metrics asset managers often draw investors' attention to. The first is downside protection, while capturing enough upside. The second is how frequently a manager has been ranked in higher performance quartiles.

The ideal fund manager is one that captures the most upside and protects from the most downside. Such a feat is of course difficult to deliver, as illustrated in Exhibit 8 below. Managers either reap a lot of upside but also suffer when markets pull back or adopt a conservative stance that cushions downside risk but fails to capture adequate upside. It goes without saying that no asset manager can constantly beat the market.

The above comparison points to Hyperion and Magellan being somewhat more competent in beating their benchmarks and delivering higher alpha than peers. Hyperion Global Growth successfully eked out above-market returns during bull markets, though the technology-sell off in

early 2022 ended its once-pristine downside capture and drawdown (peak-to-trough decline) track record. Regardless, its trailing three-year performance has consistently been in the top quartile over the last 48 months, which helps it continue attracting new money.

Magellan Global is a close second, ranking in top quartile 84% of the time over the last 12 years. The strategy's low drawdown metric is a clear standout to competitors. This was despite Netflix and Meta—its concentrated bets—having been significantly de-rated by the recent technology sell-off. The strategy's balance between structural growth and defensive businesses (that should generate predictable cash flow), holdings in large firms with global operations (meaning more diversified revenue streams), and high cash levels (that can reach up to 20%) are features Magellan has historically exhibited to minimise portfolio volatility.

Importantly, Hyperion and Magellan support our thesis that holding undervalued, moaty stocks helps generate alpha and reduce portfolio volatility.

The subpar track records for both Platinum Global Long Only and Antipodes Global Fund - Long speak to the burdens contrarian investors must bear. Their distinct value biases relative to the benchmark mean they are best used as a supporting player, that is, not the bulk of an investor's portfolio. The case with both managers suggests supporting players may be better owned by a holding company (as is the case of Antipodes with Pinnacle), rather than operating as a standalone boutique like Platinum.

Notwithstanding Antipodes' relative underperformance, Pinnacle has packaged its value-oriented funds with other growth strategies (within Pinnacle's portfolio) and sold them to investors who want a blended style. We think being backed by a growth incubator—who is known for partnering with high-quality managers and can provide optionality to investors—like Pinnacle increases Antipodes' odds of winning new money, than if it were to go it alone as Platinum does. As demonstrated in Exhibit 7, a portion of Antipodes' strategies are in net inflows despite its patchy track record.

The first challenge for contrarian investors is waiting for the market to also buy into their contrarian ideas. The absence of this could mean that they tread water. This is evidenced by the relatively low top quartile frequency (and high lowest quartile frequency), as well as the low upside capture for both Platinum and Antipodes' long-only strategies. The second challenge is facing the possibility their contrarian bets are indeed wrong and the investment backfires. As above, both strategies don't appear to deliver much lower drawdowns despite being valuation-focused, which should offer a margin of safety that cushions against major losses.